I had to change the name of my blog. Why? Because the new CEO is the future of business.

Over the past couple of months, I’ve talked with CEOs and I’ve noticed a sea change in the challenges and opportunities they’re grappling with, including a:

- Shift from shareholder value to stakeholder value that requires authentic corporate social responsibility engagement with consumers and the community.

- Seismic demographic, ethnic, and gender transference is underway from Baby Boomers to Gen X, Millennials, and Gen Z as leaders, employees, entrepreneurs, and consumers.

- Reimagination of physical products and services to digital products and services is critical to disrupting your own products before the competition does.

- Recognition that understanding behaviors, not transactions, is redefining customer relationships.

- Realization that we’re in a Gilded Age where there is a veneer that everything is great and we’re experiencing a movement to an Authenticity Age where a new generation of leaders, consumers, and community are seizing the opportunity to solve the challenges we face by establishing a social business or adding a corporate social responsibility component to their business.

The New CEO

The New CEO. Photo Credit: Canva.

What’s abundantly clear to me is a new type of CEO has arrived and we need to understand how the role is being redefined. As the focus shifts to stakeholders, the next generation, digital, behaviors, and social business, companies have to rethink their business strategies or else they could be out of business.

The new CEO requires a different set of skills and capabilities to address these innovative opportunities. That’s why I’ve renamed my blog and newsletter “The New CEO” to create a space for exploring these ground-breaking changes.

The New CEO of today is:

More diverse than ever before. Whether the company is a publicly or privately held company, CEOs and Founders are increasingly ethnically diverse.

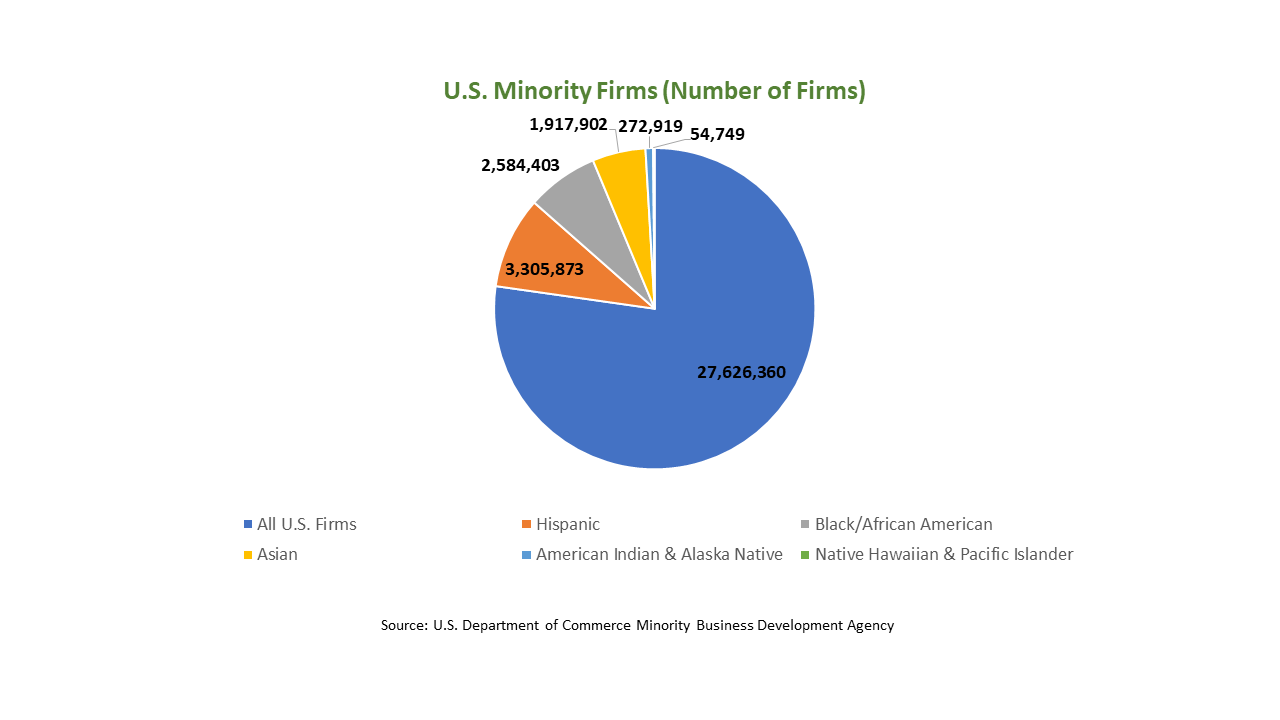

In the SMB space, the number of minority-owned businesses has increased by 38% since 2007, generating $1.4 Trillion in revenue. Middle Market firms, in the $10 Million to $1 Billion space, that are minority-owned now represent 5% of the total market of an estimated 137,000 companies in the U.S.

A woman changing the company direction. While the number of businesses headed by minority CEOs is growing, so are the number of women CEOs. Women started an average of 1,821 new businesses per day in the US between 2017 and 2018. In the Middle Market space, 13% of companies are women-owned business or women-led businesses. Six percent are majority owned women-owned businesses. For Large Cap companies on the S&P, women represent 5.6% of CEOs and growing.

A prime example of this is TaskRabbit, a middle market firm known for enabling customer to go online and hire freelancers to do deliver groceries, mount wall TVs, to put furniture together. Stacy Brown-Philpot joined TaskRabbit, succeeded Founder Leah Busque, as the company CEO and put together a partnership IKEA furniture to help customers put their furniture together. In 2017, IKEA saw the value of the partnership and acquired the company. Brown-Philpot continues to lead the company the CEO and is taking TaskRabitt/IKEA services into additional countries.

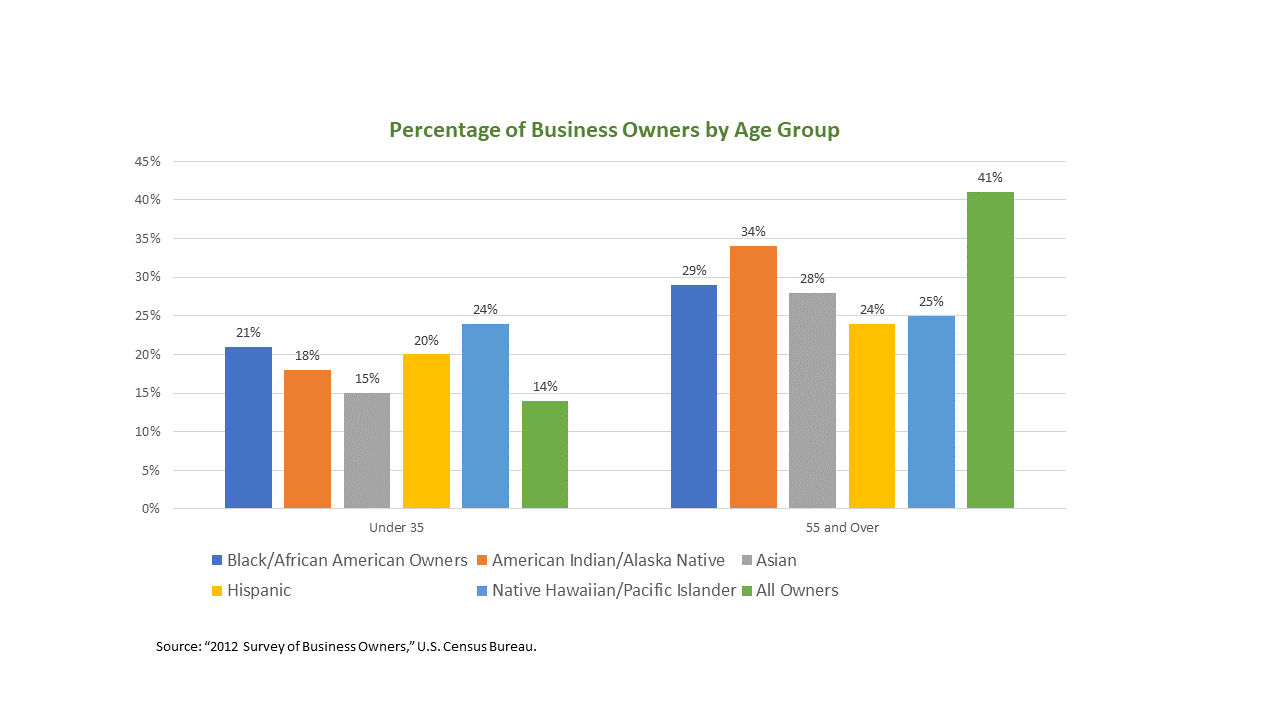

Defying age limits. In addition to the gender and ethnicity, the age of CEOs is changing. The average age of entrepreneurs in the U.S. is 45. Fifty-four percent of all small business owners are over 50 years old and 66% of men over the age of 50 are starting businesses. Women-Owned Business owners account for 48% of the business owners between the ages 45-65 years old. Thirty-one percent are between 25 and 44 years old.

In 2005, at the 65 years of age, David Duffield started Workday, a cloud-based human resource and finance solution for enterprise businesses. The company went public 2012, with a market cap of $26.47B. For Duffield, this wasn’t his first business, but his second. He cofounded PeopleSoft after the age of 40 and it was acquired in a hostile takeover by Oracle. He proved he could do it again.

Analytics. Photo Credit: Canva.

Digging deep into the analytics behind customer behavior. With the quickening pace of new industry disruptors, changing customers, and cheaper technology lowering the barriers to entry for new competitors, CEOS are rethinking their business strategy. And, they’re realizing the way customers are changing isn’t just a demographic shift, it’s a behavioral shift.

Mattel’s Hot Wheels has been the number one toy sold globally for the past 50 years. Yet, for the last four years, Ynon Kreiz, Mattel’s CEO, dug into the analytics. The topline data indicated the company sold 500 million Hot Wheels in 2018 and on average a child owns 50 cars.

Hot Wheels. Photo Credit: Canva.

Kreiz also knew 92% of children between 3 and 12 years old already had a digital device. By age 6, the time a child spent on physical toys was slightly more than the time spent on digital toys. But by age 8, the time spent on digital toys exceeded that of physical toys. The question he had was how to use this behavioral shift to ensure Hot Wheels would be around for another 50 years?

Embracing the analytics, Kreiz partnered with ApplePay to deliver an integrated physical and digital experience for his customers. In 2019, Hot Wheels iD and a Hot Wheels iD Smart Track products where introduced. The addition of a communications device attached to the car allows users to pay to track on their phone the speed of the car, mileage, car specs, and car combinations running on the track. This new solution created an incremental revenue stream for both Apple and Mattel, maintained product relevance, and enhanced a customer experience for the customer.

Taking a nonlinear path to reach new customers. The employees and customers of today have multiple choices available to select who they will work for and do business with. One criteria moving up the checklist is the Corporate Social Responsibility. Many potential employees, partners, and customers are more interested in what the company stands for beyond their products and services. They want to know how they align with and support the community.

For Jacquie Berglund, Co-Founder and CEO of FINNEGANS Brew Co., it’s about turning an experience of growing up in a financially struggling family into a mission to feed others. Her business strategy was to establish FINNEGAN Brewery in Minnesota to create and sell beer to stores, customers, and wholesalers.

Produce. Photo Credit: Canva.

All of the profits generated from the brewery are then contributed to FINNEGAN Community Fund, a 501 (c)3 nonprofit. The nonprofit provides funding to community food banks in the states the brewery operates in to purchase produce and make it available to those in need. In short, FINNEGANS sells beer to feed people. It also invests in other local social businesses through their FinnovationLab to pay it forward to help other nonprofits to get off the ground.

Are You A New CEO?

The New CEO blog will explore these and other changes through monthly interviews with CEOs and Founders. We’ll talk about the challenges they’re taking on and the innovative ways they’re finding to master the skills and capabilities their companies need to grow. Join us on this journey.

You must be logged in to post a comment.